Stylam Industries Limited (India) enters into strategic partnership with Aica Kogyo Company, Limited (Japan) to create one of Asia’s Premier Laminates and Surface Solutions Leader. Aica to acquire atleast 40% stake for USD ~170 mn to ~225 mn in Stylam.

Raj Shroff is the Founder and Director of Aarayaa Advisory Services. He has more than 2 decades of professional experience in mergers and acquisitions, capital raising, joint ventures, international tax, merchant banking and valuations with being associated with closure of more than 100 deals. He is also Partner, Managing Director of The Corporate Finance International Group – India. He is also associated with V. B. Desai Financial Services Limited – a Category I merchant banker which has handled more than 100 public offerings. He is also registered under Insolvency and Bankruptcy Board of India (IBBI) asRegistered Valuer (Securities or Financial Assets).

Prior to the founding Aarayaa, Raj was heading the globalisation practise at one of the leading law firms in India – Nishith Desai Associates.

He is a fellow member of Institute of Chartered Accountants of India and a Certified Public Accountant from California, USA.

Raj is a visiting faculty at Government Law College. Raj has written numerous articles and is also a frequent speaker at various professional and trade association.

Hoshi Deboo is Founder and Managing Partner of Ahura Global Partners based in Singapore.

He has been a senior executive with over 35 years of US & Asia Pacific experience in growth and turnarounds across wide industry segments and with publicly listed and private companies. He advises and provides investment life cycle advisory services to middle market investors and companies and also co-invests. He assists companies and investors with deal screening, restructuring, reinvent business and M&A advisory to leverage over 3 decades of operating and funding experience in several industry segments.

Hoshi holds a B.TECH (HONS) in Mechanical Engineering from the Indian Institute of Technology, Kharagpur, India and a Master of Science in Industrial & Systems Engineering from the Illinois Institute of Technology in Chicago, Illinois, USA.

CFI-India is pleased to announce that it acted as exclusive financial advisor to AmpVolts in raising debt funding from SBI, supporting strategic growth initiatives in the renewable energy sector.

The CFI Group acted as the exclusive financial advisor to Robertet Group in its divestment of Sirius to Associate Allied Chemicals (AAC) and Nikunj Harlalka.

Aarayaa – CFI India acted as the sole financial advisor to Maple Press on its strategic investment from Penguin Random House India.

Bharat has three decades of professional experience, across the full spectrum of Private Equity and Venture Capital – from fund set-up to liquidation. His career spans investment evaluation, due diligence, deal structuring, portfolio monitoring, value creation, and successful exits, having led 30+ business sale and exit transactions valued at over US $300 million (INR 2,500+ Cr).

As a Super CFO, Independent Director, and turnaround specialist, he has been instrumental in driving business transformation, forging strategic partnerships, and leading high-stakes negotiations

CFI Group is pleased to present the Specialty Chemicals Valuation Snapshot for the first semester 2025. This report provides commentary and analysis on current market trends and M&A activity within the Specialty Chemicals sector.

Spotlight

The first half of 2025 has been difficult for Europe’s chemical industry. Output fell by over 2%, utilisation rates stayed well below average, and high gas prices — almost three times US levels — continued to erode competitiveness. Weak demand from automotive and construction sectors, combined with faster-growing imports, cut the region’s trade surplus sharply. Without relief on energy costs or stronger downstream recovery, Europe risks losing further ground globally.

India, by contrast, remained resilient. Strong domestic demand and rising exports in specialties kept growth intact, supported by government policy and new capacity additions. Indian producers are moving up the value chain and benefiting from global buyers diversifying supply chains away from China.

The US sector stayed stable, supported by low-cost shale gas and steady demand from industrial and consumer markets. Abundant feedstock supply helped keep utilisation high and costs competitive, reinforcing its structural advantage over Europe.

China led global growth, with chemical output up nearly 8% in H1. Government support, recovering manufacturing demand, and strong performance in electronics, batteries, and infrastructure-related segments kept momentum high, even as challenges in real estate lingered.

Globally, chemical production still grew by around 4% in H1 2025, but growth was concentrated in Asia and the US, while Europe lagged. The divergence between cost-advantaged and cost-pressured regions is becoming more pronounced.

Global Outlook

M&A activity reflects this shift. Deal volumes have declined, but average deal size is up, with companies pursuing fewer but more strategic moves. The focus is on “divest-to-invest” strategies, freeing resources for specialties, advanced materials, and sustainable technologies. Asia has been the most active region for such deals, while Europe remains subdued. Going forward, value creation will hinge less on scale and more on sharper portfolios, operational discipline, and positioning in high-growth, innovation-led markets.

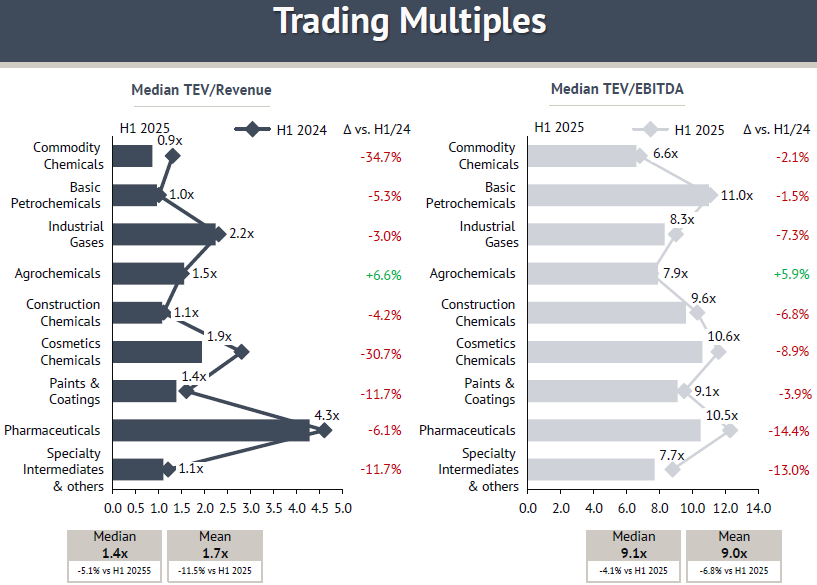

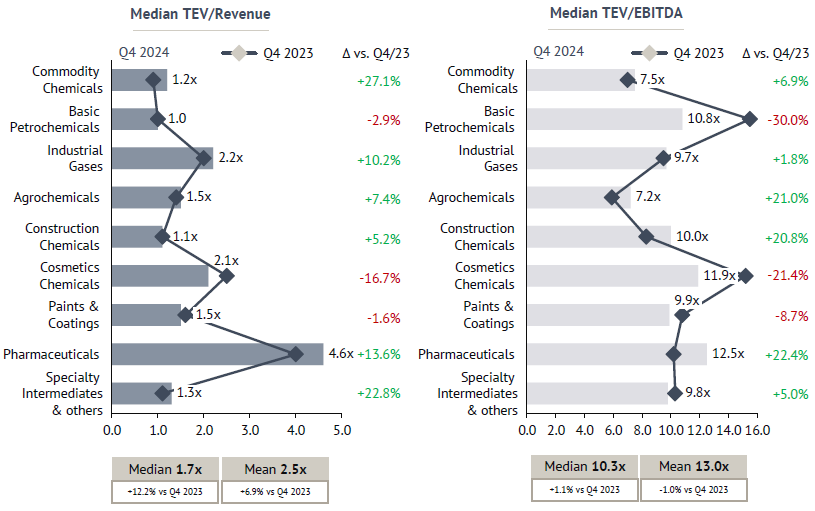

H1/25, trading multiples in the chemicals sector declined, reflecting weaker investor sentiment driven by slower global growth, renewed U.S. tariffs, and geopolitical uncertainty. With U.S.-listed companies making up a substantial portion of the dataset, the reported valuation trends are particularly sensitive to American policy shifts and investor sentiment. The median TEV/Revenue fell to 1.4x (-5.1% YoY), while the median TEV/EBITDA dropped to 9.1x (-4.4% YoY). This signals that equity markets are pricing in lower growth and profitability expectations across much of the industry.

The sharpest repricing occurred in Commodity Chemicals, where TEV/Revenue multiples fell from 1.4x to 0.9x (-34.7% YoY). This shows that investors are assigning very limited value to sales in a segment heavily exposed to cyclical swings and international trade flows. Cosmetics also performed poorly, with TEV/Revenue multiples falling -30.7% YoY and TEV/EBITDA down -8.9% YoY, highlighting the impact of weak consumer demand. In contrast, Agrochemicals was the only subsector to post gains, with TEV/Revenue up +6.6% and TEV/EBITDA up +5.9% YoY, supported by resilient food demand and defensive business models.

Pharmaceuticals, which previously led sector valuations, corrected as well. TEV/Revenue declined -6.1% YoY, while TEV/EBITDA fell -14.4% YoY, suggesting a normalization after several strong quarters. Industrial Gases posted more modest declines, with TEV/Revenue down -3.0% YoY and TEV/EBITDA down -7.3% YoY.

The drop indicates that, despite supportive long-term demand in energy and industrial end-markets, near-term pricing pressure has begun to weigh on investor expectations. Basic Petrochemicals (-5.3% in TEV/Revenue) similarly showed signs of valuation pressure.

Construction Chemicals and Specialty Intermediates also reported declines across both valuation metrics, pointing to weaker building activity and softer demand in industrial supply chains. These results underline that the pressure on trading multiples is broad-based, sparing only a few of more resilient subsectors.

Looking ahead, the sector faces a challenging environment. The new U.S. tariffs on imports, particularly from Europe, are disrupting global trade flows and creating uncertainty in investment planning, especially due to the chemical heavy-weights sitting in DACH-Area. Combined with softer macroeconomic indicators and the risk of recession in key markets, these factors weigh on profitability expectations. Still, subsectors with stable or counter-cyclical demand, such as Agrochemicals, are expected to remain more resilient. Overall, the sector has underperformed, with valuations remaining under pressure. A recovery could emerge once companies and investors adapt to new tariff structures and recession fears ease, provided geopolitical uncertainties are gradually resolved.

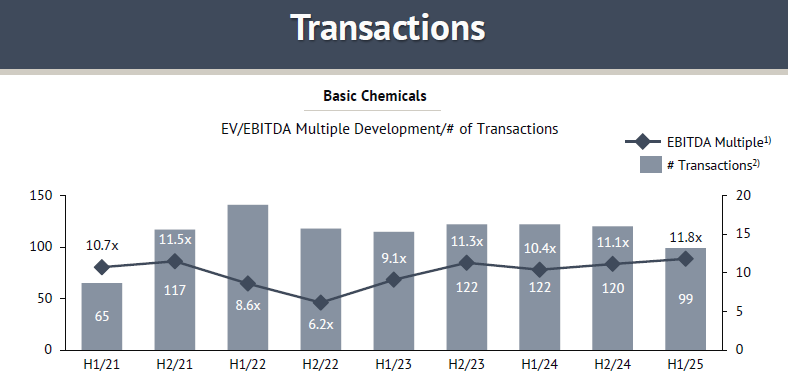

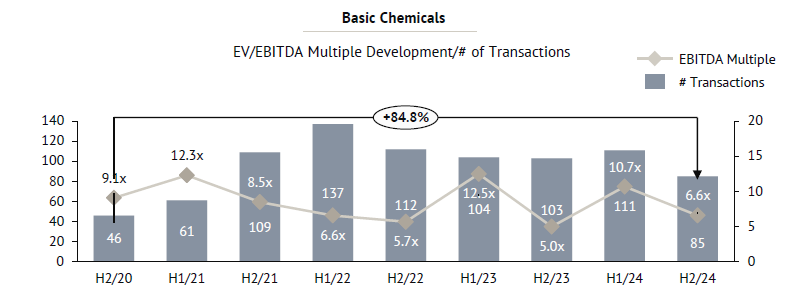

In H1/25, M&A activity in Basic Chemicals slowed further, with 99 announced transactions, down from 120 in H2/24 and well below the H1/22 peak of 141. By contrast, valuations strengthened: the median disclosed EV/EBITDA multiple rose to 11.8x, the highest level observed across the last nine semesters and above the 11.1x recorded in H2/24.

This divergence underscores the selectivity of current market dynamics. While overall deal volumes remain under pressure, competitive tension for resilient and strategically relevant businesses continues to drive disclosed multiples higher. The sharp rebound from the 6.2x trough in H2/22 illustrates the volatility of a small disclosure base, yet the consistent return to double-digit levels since 2023 indicates that investor appetite for quality assets has not structurally weakened.

At the same time, the sector remains exposed to persistent structural headwinds. Regulatory requirements, rising input costs, and trade frictions – particularly U.S. tariffs – are compressing margins and weighing on broader market sentiment. Against this backdrop, H1/25 highlights a disciplined M&A environment, where buyers are cautious on volume but willing to pay a premium for differentiated Basic Chemicals platform.

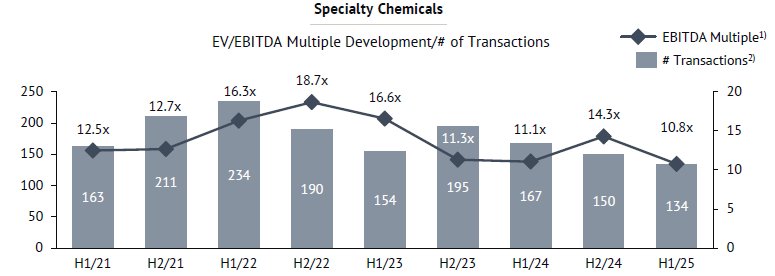

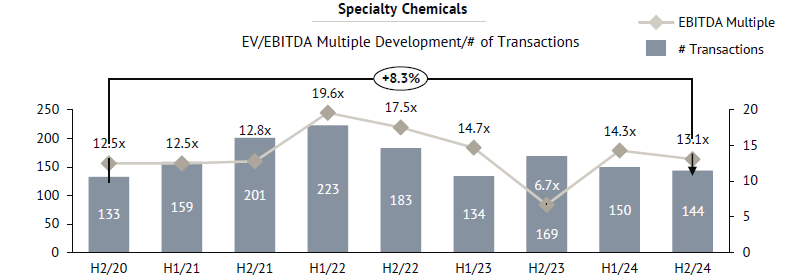

In H1/25, median EV/EBITDA multiples in the Specialty Chemicals sector declined, marking a sharper correction compared to the relative stability observed in 2024. With 134 deals announced, activity remained lower versus H2/24. The median multiple decreased to 10.8x, the lowest level since 2021, pointing to a more cautious valuation environment.

The decline reflects an easing of the momentum that had gradually returned in 2024, as financial sponsors continue to reassess pricing discipline amid broader market uncertainties. Nevertheless, private equity remains a key driver of activity, supported by ample dry powder and continued appetite for add-on acquisitions. While premiums for high-quality assets persist, the narrowing of headline multiples suggests that investors are focusing on operational resilience and profitability rather than paying for growth alone.

Looking ahead, the role of financial investors in shaping deal activity is expected to remain significant, though with greater selectivity. This shift could further accentuate the polarization of valuations between best-in-class Specialty Chemicals businesses and more commoditized assets.

Global Deal Activity – Overview

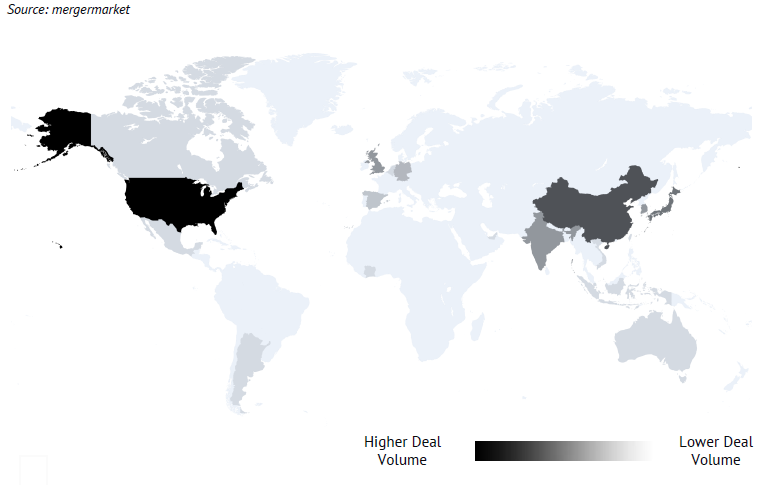

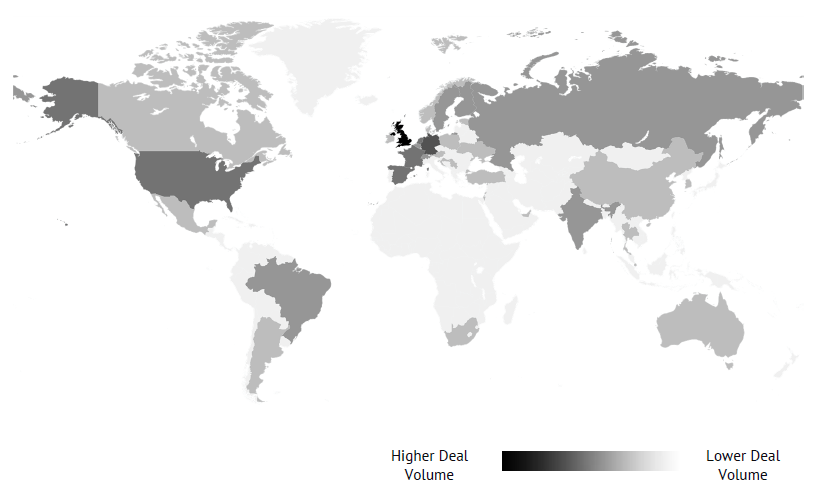

In the global M&A landscape across specialty and basic chemicals, deal activity in H1 2025 was led by the United States, which recorded the highest volume of transactions. A favorable cost environment, strong capital availability, and steady demand across industrial and specialty markets reinforced its position as the most active hub. Private equity participation remained significant, and portfolio reshaping continued to drive deal flow.

China and India followed as key centers of activity. China benefitted from strong industrial demand, government support, and ongoing interest in high-value segments such as advanced materials and sustainability-linked solutions. India maintained resilience through strong domestic consumption and rising interest from global buyers seeking diversification and access to its fast-growing market.

South Korea, Japan, and Southeast Asia registered moderate activity, largely in technology-driven and specialty segments, reflecting the region’s focus on innovation and advanced materials.

Europe showed more restrained deal-making. While Germany, Italy, and the UK remain relevant players, high energy costs, regulatory complexity, and subdued demand weighed on overall volumes. Transactions were concentrated in selective niches rather than broad-based consolidation.

Latin America remained lighter in volume, with Brazil and Mexico leading regional transactions, particularly in agrochemicals and industrial applications. The Middle East and Africa featured smaller but notable deals, with the UAE consolidating its role as a cross-regional hub and South Africa contributing resource-linked activity.

Overall, the United States emerged as the clear leader in global chemical M&A by volume, with China and India as the next most active markets. Europe stayed subdued, while Latin America, the Middle East, and Africa presented selective, sector-specific opportunities.

CFI Group is pleased to present the Specialty Chemicals Valuation Snapshot for the second semester 2024. This report provides commentary and analysis on current market trends and M&A activity within the Specialty Chemicals sector.

Spotlight:

The chemical sector continues to navigate challenges posed by geopolitical tensions, economic uncertainties, and input cost. In particular, new regulations mandate the use of higher-cost approved materials to replace lower-cost prohibited ones, further straining the cost structure of the industry. However, recent earnings reports indicate a steady recovery in sales volumes, with companies like Arkema reporting improvements as destocking trends subside. Firms have shifted focus from price competition

to operational efficiency, with e.g. Brenntag optimizing costs and operational footprint to enhance profitability.

M&A activity has remained robust, driven by portfolio realignments, consolidations, and strategic acquisitions. Notable deals include BASF’s sale of its Flocculants business to Solenis and the portfolio realignments of Hempel (sale of JW Ostendorf and Schaepmans). Specialty Chemicals have seen strong demand from engineering and semiconductor industries, with the global semiconductor market projected to grow 16% in 2024, fueled by AI and battery electric vehicles advancements.

Looking ahead, the chemical industry is expected to expand at a slower pace than historical trends, facing continued uncertainty from geopolitical shifts and regulatory pressures. However, stable inflation and falling interest rates may fuel M&A activity in 2025, with corporate restructuring and PE investments driving deal flow. PE firms, pressured to deploy capital and monetize assets, may pursue larger transactions as well as add-ons, potentially shaping the industry’s next phase of consolidation.

Global Outlook:

The global chemical industry in 2025 will be shaped by economic pressures, sustainability initiatives, and digital transformation. Our own guess is that economic growth and with it deal activity will significantly

pick up in 2025. While some regions face cost inflation and demand fluctuations, others are leveraging efficiency improvements, high-value product innovations, and strategic production shifts. The market is

projected to reach USD 6.3 trillion, driven by advancements in green chemistry, circular economy practices, and resilient supply chains. Companies worldwide are investing in automation, AI-driven operations, and eco-friendly solutions to enhance competitiveness and long-term growth in an evolving regulatory and consumer landscape.

After a substantial increase in valuation multiples in H1/24, both TEV/Revenue and TEV/EBITDA multiples continued to improve in Q4/24, albeit at a slower pace than the surge observed between Q2/23 and Q2/24. Median TEV/Revenue rose by +12.2% YoY, while TEV/EBITDA increased by +1.1% YoY (Q4/23 vs. Q4/24).

The Commodity Chemicals sector experienced the most significant rebound in TEV/Revenue multiples, rising from 0.9x to 1.2x (+27.1% YoY), although on a low level. In contrast, the Cosmetic Chemicals sector saw a decline in TEV/Revenue multiples (-16.7% YoY), reflecting ongoing challenges in demand.

Median TEV/EBITDA multiples generally showed an upward trend, though sectoral variations persist. Agrochemicals posted a substantial increase from 5.9x to 7.2x (+21.0% YoY), second only to Pharmaceuticals, which saw a +22.4% YoY rise. Conversely, Cosmetics Chemicals, Paints & Coatings, and notably Basic Petrochemicals (-30.0% YoY) deviated from this trend, recording declining multiples.

Previously, Basic Petrochemicals held the highest TEV/EBITDA multiples, but Pharmaceuticals have now surpassed them, also leading in TEV/Revenue multiples. Analysts highlight that pharmaceutical companies still maintain significant capital reserves, which they may deploy as opportunities arise, particularly with advancements in AI opening new avenues for growth and efficiency.

The decline in Basic Petrochemicals’ TEV/EBITDA multiples coupled with only a slight decrease in its TEV/Revenue multiple compared to Q4/23, suggests a potential decrease in profitability expectations following a challenging economic environment, particularly in China. This trend may indicate lingering pressures despite overall early signs of recovery.

Construction Chemicals and Specialty Intermediaries reported notable increases in TEV/EBITDA multiples (+20.8% and +5.0% YoY, respectively). Their TEV/Revenue multiples also rose, with Specialty Intermediaries experiencing a stronger surge in their TEV/Revenue multiple (+22.8% YoY). This pattern mirrors developments in Basic Petrochemicals, indicating modest market improvements that are not yet fully reflected in the M&A and stock markets.

Similarly, Industrial Gases followed the trend of Specialty Intermediaries, showing a significant increase in TEV/Revenue multiples (+10.2% YoY) alongside a modest rise in TEV/EBITDA multiples (+1.8% YoY). This suggests growing profitability, supported by favorable global industrial and energy market conditions.

Looking ahead, the chemicals sector faces a complex landscape heading into 2025. Potential shifts in U.S. political policies favouring industry could drive valuation multiples higher, signaling growth prospects and enhanced profitability. However, newly introduced tariffs and trade barriers generally hurt the chemical industry significantly. Despite these challenges, a cautious optimism prevails, with expectations of a gradual market recovery on the horizon.

In H2/24, median EV/EBITDA multiples in the Basic Chemicals sector declined, with a drop in transaction volumes. While volumes remain above the all-time low caused by the pandemic, they have yet to recover to peak levels observed in H1/22. With fewer transactions with disclosed multiples, data has become more volatile, leading to significant fluctuations in recent periods.

At the same time, the decline in the median EV/EBITDA multiple in H2/24 suggests that ongoing challenges faced by chemical companies persist. Some of the previous market momentum in H1/24 appears to have cooled, particularly as the Basic Chemicals sector benefits less from private equity interest compared to Specialty Chemicals firms.

Additional pressures stem from shifting customer preferences, with an emphasis on decarbonization, which negatively impacts profitability. As a result, investors are gravitating toward higher-margin Specialty Chemicals businesses, further weighing on valuations in the Basic Chemicals sector.

As in H1/24, the sector remains defined by fluctuating transaction volumes and evolving market dynamics in H2/24. With a growing focus on sustainability and cost efficiency, the trend of acquiring high-quality Basic Chemicals firms may become more pronounced.

The M&A landscape in the Specialty Chemicals sector has remained relatively stable, with only a slight decline in multiples compared to H1/24. However, in 2024 transaction multiples appear to have gained some momentum compared to 2023 – a trend driven in part by the growing interest of financial investors in the sector.

As highlighted by The Argos Index®, which tracks mid-market transactions, financial investors continue to pay higher multiples than strategic buyers as observed in H1/24. This highlights the sustained and growing interest of private equity, additionally driven by the significant amount of available “dry powder” and the increasing number of LBO transactions.

While the gap between the lowest and highest paid multiples widened last year, this trend appears to be continuing, reflecting growing valuation disparities and increasing premiums. However, these observations should be interpreted with caution, as data on recent transactions in the Specialty Chemicals sector, particularly in the mid-market, may be distorted due to limited disclosure.

Looking ahead to H1/25, private equity is expected to pursue add-on acquisitions, building on their platform investments. This trend will continue to shape the M&A landscape and support transaction volumes

Global Deal Activity –Overview

In the global M&A landscape across specialty and basic chemicals, distinct regional trends continue to shape the market.

The United Kingdom, Germany, Italy, and the United States continue to be dominant players in global M&A activity, with strong deal volumes particularly in pharmaceuticals and specialty chemicals. A stable economic environment and ample financial capital, especially from private equity, drive transaction momentum. However, evolving trade regulations and political uncertainties in the U.S. and parts of Europe could introduce potential volatility in deal-making.

China, Japan, India, and South Korea exhibit moderate M&A activity, shaped by distinct economic conditions. While China faces challenges such as declining valuation multiples in certain chemical sectors, private equity interest remains robust in high-margin specialty chemicals. India and South Korea demonstrate steady growth, fueled by industrial demand and an expanding market for advanced materials. Japan, while traditionally conservative in deal-making, remains an active participant, particularly in technology-driven sectors.

Brazil and Mexico lead M&A transactions in Latin America, though overall deal volume remains lower compared to North America and Europe. Agrochemicals and industrial gases emerge as key sectors driving investor interest. Regulatory shifts and economic stability shape investment sentiment, with strategic consolidations and cross-border expansions presenting selective opportunities for growth.

The UAE, Israel, and South Africa feature in the M&A landscape, reflecting growing deal activity in energy, specialty chemicals, and pharmaceuticals. The UAE’s business-friendly policies and financial infrastructure establish it as a hub for cross-regional transactions. Meanwhile, Africa remains a smaller player, though resource-driven industries and infrastructure deals continue to attract international investor interest.

Source: Merger Market

•India is the world’s 3rd largest automotive market, only behind China and the USA, with Passenger Vehicles (PVs) domestic sales of ~4 mn units and exports of ~0.7 mn units in FY24. The total production output across segments was ~29 mn units in the same year.

•The industry plays a pivotal role in the nation’s economic landscape, contributes 6% to India’s GDP.

•This industry serves as a significant driver of employment generating employment to nearly 32 mn people in India.

Trends Shaping the Automotive Industry in India

•The rising disposable income of a growing middle class, combined with a market that has a low automotive penetration rate is driving demand for premium and feature rich automotive models in both 2 Wheelers (2W) and 4 Wheelers (4W) segment.

•India’s strategic initiatives including the longstanding “Make in India” campaign and other supporting policy initiatives such as Automotive Mission Plan 2026 and the National Electric Mobility Mission Plan 2030 to enhance its manufacturing capabilities.

•Favorable government policies and initiatives such as Product Linked Incentive (PLI) scheme launched in 2020 across 14 industries and with a total outlay of $~34 bn which provide benefits including subsidies and tax rebates to incentivize companies to invest in EV production.

•India’s expanding position as the Global R&D Hub is a key facilitator of advancement in automotive technologies and auto components manufacturing.

Automotives: Growth & Segmentation

•The automotive industry is expected to clock 4.5-6.5% CAGR between FY24 to FY29 period to reach 5.2-5.7 mn domestic vehicle sales.

•In tandem with the expansion of the automotive market, the auto component segment is expected to grow from $70 bn in FY23 to $200 bn by FY26. About $30 bn (~15%) of this is expected to be generated from exports.

•India had 26 cars per 1,000 people as of FY24. a significantly lower penetration than developed nations and even emerging nations like Brazil (214), Russia (389), and Mexico (358). This provides significant headroom for growth, given the expected increase in disposable incomes, faster economic growth, younger population, and increased focus from international OEMs.

Market Segmentation

•The automotive sector is split into four segments i.e., 2W, 3W, Passenger Vehicles (PV) and Commercial Vehicles (CV), each having few market leaders.

•In FY23, 2Ws and PVs held a market share of 75.4% and 17.7%, respectively. India is the largest 2W market in the world, given their low ticket size compared to PVs, however there is a clear rise observed in market share of PVs in the post covid recovery of automotive sales.

•Within PV segment. there is a clear shift in consumer preferences observed with increasing preference for Utility Vehicles over Hatchbacks and Sedans which is attracting international OEMs to bring more premium models to the Indian market

•Furthermore, a premiumization trend is observed through consumer demand for vehicles with Enhanced Safety Features (Anti Braking systems, ADAS), Connected devices, Cutting edge Infotainment Systems, Sunroofs and Aesthetic interiors

Electric Vehicles: Current Landscape

•The Electric Vehicle (EV) market in India is expected to grow at a CAGR of 49% between 2022-2030 presenting a massive investment opportunity of over $ ~200 bn over the next 8-10 years.

•Factors driving electrification in India:

•Government Subsidy (e.g., FAME $ ~320 mn (FY24), Production Linked Incentives – $ ~6 bn for automotive industry)

•Awareness of Environmental Issues

•Expansion of Charging Infrastructure

•Availability of EVs at Competitive Prices

•Disruptor brands are currently dominating market share in both E2W (Ola & Ather) and E-PV (Tata Motors & Morris Garage).

•EV adoption in India is being led by E2Ws owing to strong supply, compact designs, limited range anxiety, smaller and lighter batteries and lower initial price difference. Premium E2Ws (priced ex-showroom >INR100,000/$1,250) had a penetration of ~75% in H1FY24.

•With the projected decline in E2W prices (led by drop in battery price), consumers are likely to see a higher number of options across price ranges, driving greater adoption in the lower price bracket as well.

•India’s current ratio of charging stations to cars is approximately 1 charging station per 135 EVs which is significantly lower than the global ratio of 1 charging station per 6 to 20 EVs.

•Furthermore, the charging infrastructure is unevenly distributed creating a significant discrepancy between the current number of EVs and the charging stations. For example, the state of Uttar Pradesh has 0.45 mn EVs, but 406 charging stations — only 1 station for every 1,103 EVs.

•To meet the government’s aim to have 30% of new private vehicles as EVs by FY30, India will need a total of 3.9 mn public and semi public charging stations for a ratio of 1 station per 20 vehicles.

•The under development of charging infrastructure is a key deterrent to EV adoption as drivers experience range anxiety while using EVs for long distance journeys or long hours of use in case of ride share and last mile delivery service players.

•While private sector players such as Tata Power, Jio–BP Charge Zone, Exicom, Finland’s Fortnum (Glida) are making significant investments in developing the infrastructure to achieve the desired ratio of stations, innovative models like battery swapping and smart charging will also improve affordability and convenience for EV owners.

Sources: SMEV, VAHAN, EV Auto, Reuters, YourStory, Bolt.Earth, Note: 1. Financial Year in India is from March to April.

Electric Vehicles: The Road Ahead

•While EVs have emerged as the leading alternative powertrain to Internal Combustion Engine (ICE) vehicles, the overall EV penetration rate (~4.4%) in India is still quite low compared to China (~40%) and the USA (~12.5%).

•In India, OEMs are adopting a multi powertrain approach by introducing new models across ICE, EV, Hybrid (Combination of ICE and EV) and Compressed Natural Gas (CNG).

•Hybrid cars popularized by OEMs such as Toyota, Honda and Maruti Suzuki are becoming a popular alternative to EVs as they solve for two main deterrents to EVs – range anxiety and limited charging infrastructure.

Case for Hybrid Vehicles: A combination of EV and ICE

•In India, Hybrids are being seen as a stepping stone to new technology bringing down apprehensions about transitioning to a full EV.

•Their reliability (no range anxiety, no faulty battery concerns), affordability (in comparison to EVs) and lesser maintenance costs (in comparison to ICE vehicles) are making them favorites amongst both OEMs and customers.

•Hybrids are seen as a viable option, in addition to EVs to support India’s COP26 goals for reduction of carbon footprint because:

•They reduce CO2 emissions by at least 30% and increase energy efficiency up to 44% in comparison to ICE Vehicles.

•Given limitations in development of charging infrastructure, shift to Hybrids from ICE will be critical in reducing emissions

•As of FY24, EVs and Hybrids have a similar market penetration in India. However globally there has been a downward trend in EV sales, while Hybrid demand is picking up. Automotive players are becoming increasingly bullish on Hybrids

•BYD, the largest global EV player currently has also increased its guidance for Hybrid sales.

•Maruti, India’s largest OEM, expects 25% of PV sales to be from Hybrids by 2030

•Toyota plans to convert most, and eventually all of its Toyota and Lexus line up to hybrid only models for its US market.

Battery Swapping : Solution for EV Charging & Battery life Concerns?

•Even though the total lifecycle cost of EVs is lower than ICE vehicles, they have a high upfront cost.

•Large proportion (35-40%) of the upfront cost is attributed to the Battery Pack. China’s Nio has successfully demonstrated that battery swapping can solve for these challenges through following strategies:

•Bring down the cost of owning EVs by offering a subscription based Battery-as-a-service (BaaS) model.

•Reduce risk of owning a faulty battery as the batteries are regularly inspected and maintained by the company.

•Users get to upgrade to the latest generation of technology without worrying about end of life hassles.

Sources: HBS, Redseeder Research, CRISIL MI&A, Economic Times, Fortune India, Note: 1. Financial Year in India is from March to April. FY24 YTD refers to Apr 2023 – Feb 2024 period.

M&A Trends and Recent Deals

M&A Activity Drivers

•In FY23, the manufacturing sector had one of the highest growth rates in M&A activity amid general market suppression, with a rise in M&A deal value in the sector by 33% and deal volume increase of 22% compared to previous year.

•The automotive sector has been a magnet for foreign direct investment (FDI), with a cumulative equity FDI inflow of about $35 bn between April 2000 and September 2023.

•There’s a noticeable interest in eco-friendly solutions and technological advancements, particularly within EV and Mobility as a Service sub-sectors.

•Emerging interest areas such as Auto Tech and Auto components indicate new opportunities for technological enhancements and market expansion.

•In Q2 2024, Domestic consolidations continued to lead M&A volumes with a 60% share while inbound activity continued to lead the values contributing to 65% of overall M&A values.

Conclusion

The automotive industry is currently being disrupted by several alternative fuel technologies – right from EV, Hybrid, Ethanol and Green Hydrogen based fuels. However, with India’s rapidly growing economy, the industry is expected to boom, irrespective of the powertrain technology, as an increase in per capita income translates to a higher vehicle penetration. In tandem, India’s strong position in both automotives and auto components, will give further impetus to companies manufacturing in and selling to India.

Opportunities exist for global companies to invest in India by providing technological expertise or by leveraging India’s manufacturing capabilities to outsource production of high quality cost competitive products. Some emerging areas of interest are battery cell manufacturing and management systems, charging infrastructure, electrical and electronics systems, infotainment systems and emission control devices.

CFI Group is pleased to present the Specialty Chemicals Valuation Snapshot for the first semester 2024. This report provides commentary and analysis on current market trends and M&A activity within the Specialty Chemicals sector.

Spotlight

•Europe remains a key region but is grappling with weak global demand and low capacity utilization. Gradual improvement is evident with EU chemical production showing steady growth since August 2023, climbing 2.4%-4.3% year-on-year (YoY) in early 2024. Though volumes are still below pre-pandemic levels, the decline of energy prices and increased demand from China signal hope for the European chemical sector’s mid-term performance. As a trading partner, however, India seems to grow in importance. Though a bit on the sideline from a pan-European perspective, the new free trade agreement established between the European Free Trade Association (EFTA) and India could be an important steppingstone for further co-operation.

•In India, the chemical sector continues to demonstrate resilience, with projected growth of 7.0%-8.0% for 2023-2024, surpassing broader economic growth forecasts. India’s recovery is underpinned by robust domestic demand, particularly after emerging from COVID-19 lockdowns. Expansionary trends in output and new orders, alongside new production capacities coming online, are set to support growth. However, market volatility, fluctuating global trade flows, and unstable upstream pricing remain concerning.

•Despite a sluggish start to M&A activity in early 2024, momentum is building. Deal volumes showed a modest recovery from the 10-year historical lows seen in 2023. Although challenges such as high borrowing costs and geopolitical tensions continue to suppress deal-making, there are clear signs of potential growth. A significant shift is expected in the second half of 2024 as central banks begin to lower interest rates, potentially unlocking more opportunities especially for financial investors. Private equity houses, still disposing of significant “dry powder”, are positioned to play an increasingly prominent role in sector consolidation. The demand for specialized products, innovation, and sustainable solutions offers promising opportunities, especially in the high-demand specialty chemicals market. As economic conditions improve and decreasing interest rates, we expect heightened competition among private equity and strategic acquirers, who have held back due to market uncertainty.

•In conclusion, despite the turbulence of recent years, the specialty chemicals sector is well-positioned for a rebound. The long-term outlook remains positive, with strategic M&A moves expected to yield significant returns. The current downturn appears to be temporary, and it is increasingly clear that the sector’s recovery is not a question of “if” but “when.“

Global Trading Multiples

After a substantial decline in valuation multiples in 2023, particularly in the first half of the year, both TEV/Revenue and TEV/EBITDA multiples showed an improvement in Q2/24. Median TEV/Revenue increased by +29% YoY, while TEV/EBITDA rose by +9.3% YoY.

The Commodity Chemicals sector saw the most notable rebound in TEV/Revenue multiples, rising from 0.9x to 1.3x (+53.4% YoY). In contrast, the Construction Chemicals sector experienced a decline in TEV/Revenue multiples (-6.3% YoY).

TEV/EBITDA multiples generally increased across sectors, but the overall picture is mixed. Agrochemicals showed a substantial jump from 3.8x to 7.8x, more than doubling its previous multiple, though from a historically low level. Basic Petrochemicals, Cosmetics Chemicals, and Paints & Coatings diverged from the trend, posting reduced multiples.

Pharmaceuticals continue to maintain the highest valuation multiples, despite previous declines. While TEV/Revenue multiples show a slight increase, expectations point to a slow rise in valuations throughout 2024. However, the potential impact of large reserves held by pharmaceutical buyers may suggest a downcycle1.

Basic Petrochemicals saw a slight decrease in its TEV/EBITDA multiple (YoY -2.7%) but an increase in its TEV/Revenue multiple (YoY +6.1%) compared to Q2/23. This suggests improving profitability after a challenging economic environment, as destocking, particularly in China2, comes to an end and demand cautiously picks up, signaling a mild recovery for the sector.

Similarly, Cosmetic Chemicals and Paints & Coatings reported declines in TEV/EBITDA multiples (-9.6% and -11.4% YoY, respectively), while their TEV/Revenue multiples slightly increased. This mirrors the trend in Basic Petrochemicals, indicating stronger profitability and suggesting modest improvements in general market conditions, not (yet) fully reflected in the M&A and stock market.

In contrast, Construction Chemicals exhibited a significant rise in TEV/EBITDA multiples (YoY +21.4%) alongside lower TEV/Revenue multiples (YoY -6.3%), bucking the trend observed in Basic Petrochemicals, Cosmetics Chemicals, and Paints & Coatings. This divergence is reinforced by the unfavorable market outlook for the construction sector in the near future3 which seems to have started in Europe, but now is spreading globally.

Looking ahead, the chemicals sector is poised for a complex landscape towards the rest of 2024. The rebound in valuation multiples for Commodity Chemicals and Agrochemicals suggests a positive trend, signaling potential growth and increased profitability. Basic Petrochemicals, Cosmetics Chemicals, and Paints & Coatings are likely to continue their gradual recovery, driven by improving market conditions and ending destocking cycles – a trend that seems to bypass the construction sector and therefore construction chemicals.

Global Transactions and Multiples

The median EV/EBITDA multiples in the Basic Chemicals sector have risen in H1/24, although transaction volumes have not returned to the peak levels observed in H1/22. Since H1/20, transaction numbers have surged by 404.5%, from the all-time low, driven by the pandemic. However, with fewer transactions disclosing their multiples in H1/24 compared to prior periods, the data has become more volatile, resulting in considerable fluctuations in multiples over recent periods.

The sharp increase in the median EV/EBITDA multiple in H1/24—more than doubling compared to H2/23—suggests a potential shift toward higher-quality assets, as fewer but more strategically significant transactions have been completed. With interest rates coming down again, larger-scale financing could become more attractive, fueling deal activity. However, chemical companies continue to face challenges as customer preferences increasingly prioritize decarbonization, adversely affecting profitability.

The sector remains characterized by fluctuating transaction volumes and shifting market dynamics. As companies focus on sustainability and cost efficiency, the trend towards acquiring strategically valuable assets is likely to persist in the near future.

The M&A landscape in the Specialty Chemicals sector has experienced a slight decline in transaction numbers, accompanied by an increase in multiples compared to H2/23. This trend is partly fueled by private equity showing stronger interest4.

The Argos Index®, which tracks mid-market transactions involving financial buyers, indicates a modest recovery in multiples5. Still, the overall trend remains downward from the record-highs in 2022. Strangely, financial investors currently seem to be paying higher multiples than strategic buyers — underscoring the increasing interest of private equity in the sector and the amount of “dry powder” available.

Data from the Specialty Chemicals sector also is distorted by limited disclosure of multiples. The mid-market experiences pronounced polarization in paid multiples, with transactions concentrated at either the higher or lower ends of the spectrum. This divergence reflects a widening valuation gap, as high-quality deals command premium prices.

Looking ahead to H2/24, private equity’s growing presence may continue to shape the M&A environment and support transaction numbers as well as multiples paid.

Global Deal Volume

Global Deal Activity – Overview

•In the global landscape of M&A activities within the specialty and basic chemicals sectors, notable trends emerge across different regions.

•In the Specialty Chemicals sector, Europe stands out with the highest number of deals, showcasing strong market consolidation and strategic acquisitions. The U.S. follows with a significant yet more measured level of activity, reflecting a stable interest in the sector. Asia, though participating at a more conservative level, shows notable contributions from countries like China, India and Japan, highlighting these markets’ growing importance in the specialty chemicals space.

•In the Basic Chemicals sector, Europe again leads the way with the most transactions, reinforcing its position as a hub for chemical industry mergers and acquisitions. While the U.S. shows significant activity, it is slightly less vigorous compared to Europe. Asia, with contributions from China, India and Japan, shows a more moderate level of activity in this sector, indicating steady engagement in the global chemicals industry.

•These trends reflect Europe’s leadership in chemical sector M&A, with the U.S. closely following, while Asian markets continue to gain momentum in both specialty and basic chemicals sectors, signaling their increasing significance in the global chemicals market.

CFI Group is pleased to present the Specialty Chemicals Global H2 2023 (Jul-Dec) Review. This report provides commentary and analysis on current market trends and M&A activity within the Specialty Chemicals sector.

• As compared to 2022, there was a significant decline in 2023 global equity market valuation in the specialty chemicals industry. It was due to a substantially weaker demand from end-use industries, de-stocking after the unclogging of the supply chains, high energy cost, intensifying recessionary effects combined with rising interest rates, and inflation. The higher cost of borrowing, which was a roadblock to deal-making in 2023, could ease amid an anticipated rewind in monetary policies. While economic drivers and market outlooks vary across the chemical industry, we see specific industry sectors with high consolidation potential — namely construction chemicals and CASE (coatings, adhesives, sealants, elastomers).

• Multiples paid in transactions also show a negative tendency with multiples dropping towards and below the 10-year historical values. Despite these effects, the number of transactions remains high in H2 2023, suggesting a sustained necessity for portfolio evaluation and strategic transactions.

• The Asia-Pacific region (APAC) again proved to be a key growth driver, though not as much as expected during the start of the year and with shifts within the region. APAC is expected to continue to hold two-thirds of the chemical market in 2024.

• Despite the hurdles faced in the global chemical market, Indian chemical companies are poised for a promising resurgence in margins. The anticipated recovery, set to materialize from the second half of FY24 will be due to a strong domestic demand and increased global interest in sourcing from India. The growing prominence of specialty chemicals and niche applications, coupled with robust capital investments by Indian chemical firms, underpins this positive trajectory. Lastly, the ‘China Plus One’ strategies employed by major customers fuel this development.

• The Global Chemical Industry is entering 2024 with a positive outlook. Despite the challenges in the past two years, the chemical industry is set to rebound with moderate growth in 2024. While challenges remain, the combined effect of rising demand and industry focus on sustainability, decarbonization, digitalization, and innovation is creating a strong foundation for growth and success in the years ahead.

• Acquirers that held back in 2023 due to uncertainty may be ready to execute in 2024. The stock market is recovering, driving up public market valuations of selling companies, and leading to more common ground in deals. With a mix of potential tailwinds and headwinds, 2024 appears poised for a cautious return to stronger dealmaking activity and higher valuations again.

• While large-scale mergers may remain elusive, increased mid-market transactions, sector-specific consolidation, and innovative deal structures will most likely define the year.

Global Trading Multiples

In 2023, specialty chemicals sector valuations fell, yet global valuation multiples rose due to a sharper decline in company profitability relative to market valuations.

The Industrial Gases sector had the most notable increase in TEV/Revenue multiples, going from 2.0x to 2.4x, whereas Pharmaceuticals and Specialty Intermediaries & others experienced a decline. Similarly, TEV/EBITDA multiples also generally increased, with Petrochemicals more than doubling its multiple from 7.0x to 15.2x, highlighting a significant jump; Cosmetics Chemicals and Pharmaceuticals bucked this trend with reduced multiples.

In terms of TEV/Revenue multiple, Industrial Gases have seen the highest increase within the last year. In 2023, the sector overcame supply chain obstacles that it had experienced in 2022. In 2023, it could position itself for future growth.

Despite high TEV/Revenue valuations in Pharmaceuticals, the sector experienced a 12.2% decline, possibly due to high-profile drug failures, and market access shifts, but still remaining on an above average level.

Due to an increase in revenues coupled with a decrease in profitability, Specialty Intermediates & others saw a decrease in terms of TEV/Revenue while simultaneously experiencing a notable increase in TEV/EBITDA multiples.

Basic Petrochemicals increased its TEV/EBITDA multiple more than 108% compared to 2022 Q4. This significant rise was not due to an increase in enterprise values, which remained steady, but rather a notable decrease in EBITDA from its all-time highs in the post-COVID raw materials price rally. Consequently, Steady enterprise value with shrinking EBITDA resulted in doubling the multiple.

Rising demand expectations for electric vehicles and renewable energy solutions are fueling growth prospects for the Commodity Chemicals sector well into 2024.Reflecting this optimism, the TEV/EBITDA multiple for Commodity Chemicals in 2023 almost doubled.

Cosmetic Chemicals have experienced a moderate decline in its TEV/EBITDA multiple. This can be attributed to the sector specific M&A environment in which strategic buyers are more dominant, looking for synergies and purely financial investors are more selective.

Global Transactions and Multiples

The global median EV/EBITDA multiple for transactions in the Basic Chemicals sector continues to trend negatively from the all-time high in 2021.

The decrease in multiples and slight decrease in transactions can be attributed to several factors. Geopolitical tension in Europe and the Middle East but also regulatory changes influence both metrics.

Even though deal activity has slightly decreased YoY, it is expected that it will increase again in 2024. The general sentiment is that the peak in interest rates has been overcome, making financing on a larger scale available again.

Chemical companies face notable pressure as customer preferences increasingly emphasize decarbonization and sustainability. Simultaneously, these companies must meet the demand for high performance and cost-effectiveness. Balancing these priorities requires strategic agility and innovation.

Overall, the M&A environment in the Basic Chemicals sector has witnessed better times. Similar to H1 2023, the industry is still facing headwinds but with more hope for 2024.

The global Specialty Chemicals’ M&A environment has witnessed an increase in transactions but a decrease in multiples for H2 2023. Part of the decrease is attributable to a statistical effect, as the number is based on a relatively small sample of transactions with published data.

The Argos Index®, which tracks transactions involving private equity, confirms the overall negative trend, exhibiting a continuous decline since 2021, with a slight recovery in 2022 before descending again to 9.0x EBITDA in 2023.

Overall, financial investors, especially private equity firms, have been and are getting more involved in the Specialty Chemicals sector. Even though there has been quite a bit of deal flow in the sector, there still are major opportunities. Private equity firms are expected to influence the M&A environment significantly in the coming years.

Similar to Basic Chemicals, the industry continues to encounter challenges, yet there is increased optimism for 2024.

As the year draws to a close, we reflect on the transformative developments strengthening the bonds between India and Switzerland. This year marked a milestone with the signing of the India-EFTA Trade and Economic Partnership Agreement (TEPA), which is set to redefine economic collaboration between India and Switzerland. TEPA stands as the first Free Trade Agreement with a commitment to targeted investments and job creation, promising to deliver $100 billion in FDI and 1 million jobs in India over the next 15 years. This transformative agreement promises to enhance bilateral trade, streamline market access, and unlock investment opportunities for businesses in both countries.

Europe’s FDI in India has reached USD 107 billion between FY 2000 and FY 2023, with Switzerland emerging as one of India’s key trade partners. Key sectors driving this trade include chemicals, precision machinery, and pharmaceuticals. Switzerland’s strong economic ties with India reflect their strategic collaboration and the growing demand for Swiss products, which underscore their quality and relevance in the Indian market.

One of TEPA’s key features is its extensive tariff concessions, covering 99.6% of India’s exports under 92.2% of EFTA’s tariff lines. Indian exporters gain 100% access to non-agricultural products, along with concessions on processed agricultural goods, while Swiss exporters benefit from reduced tariffs on 95% of industrial exports to India.

TEPA also establishes Switzerland as a strategic base for Indian businesses to access EU markets, given that 40% of Swiss exports are EU-bound. With 128 Swiss sub-sectors covered, the agreement encourages sectoral collaboration in key industries such as chemicals, pharmaceuticals, and precision machinery. Switzerland’s robust trade ties with India are underscored by its position as India’s largest European import partner, accounting for $21.24 billion in imports during FY23-24. While Chemical sector supports India’s exports and engineering products dominate India’s imports, reinforcing a mutually beneficial trade dynamic. This partnership not only highlights the quality and importance of Swiss products in Indian markets but also underscores India’s rising influence as a global trade hub.

Currently, over 300 Swiss corporations operate in India, and TEPA’s provisions are set to encourage not only more large companies but also SMEs to tap into India’s rapidly growing market, projected to grow by 6-9% annually. In a nutshell, TEPA is poised to catalyse economic synergy, fostering innovation, investment, and sustainable growth for both nations. With its far-reaching implications, this agreement strengthens India and Switzerland’s commitment to building a future of shared prosperity. We look forward to seeing the continued success of this economic partnership.

India is deeply committed to its transition away from traditional fossil fuels and building its non fossil fuel capacity to at least 500 GW by 2030. The country’s cumulative renewable energy capacity totals to 209.4 GW as of December 2024, with solar energy contributing 47% of the capacity, followed by wind energy (23%) & Large hydro Projects (22%), and the rest being generated through Bio Power (5%) and Small hydro projects (3%).

The rapid expansion of renewable energy capacity will drive higher penetration of renewables into the power grid, which may lead to grid stability challenges. At 20% penetration, grid stability becomes more difficult to maintain, while at 30%, instability becomes a significant concern. Coupled with the intermittent generation patterns of solar and wind energy, this poses a critical challenge for the Indian government in achieving its 2070 net-zero emissions target.

Energy storage systems (ESS) play a crucial role in smoothening out this intermittency and enabling a continuous supply of energy when needed. Thus, for sustainable renewable energy growth, a concurrent growth of ESS capacity is imperative. In line with this, the recent statement by Mr. Prashant Singh, Secretary of the Ministry of New and Renewable Energy, indicates that the government may mandate 10% battery storage for new renewable energy projects, which is expected to further accelerate growth in the ESS sector.

Energy Storage Systems

Energy Storage Systems (ESS) are designed to store surplus energy generated from renewable sources, which can be deployed during periods of peak demand. ESS are crucial for stabilizing the grid by reducing fluctuations in renewable energy generation. They store energy for use during peak demand, support grid stability, and enable greater renewable energy integration. ESS also help reduce peak energy costs, lower carbon emissions, defer infrastructure investments, and enable energy trading, contributing to a more efficient and sustainable energy system.

Battery-based Energy Storage Systems (BESS) and Pumped Hydro Storage (PHS) are the most widely used and commercially viable storage solutions. While other technologies exist, BESS and PHS dominate the market and are expected to complement each other, each playing a key role in supporting renewable energy growth and enhancing grid stability.

Growth Potential

The Ministry of New and Renewable Energy (MNRE) has prescribed state wise Renewable Purchase Obligations (RPOs) which mandate specified percentage of electricity to be sourced from Renewable Energy sources for Distribution Companies (DISCOMs). Similarly, Energy Storage Obligations (ESO) have been prescribed to secure grid stability, as the share of RE goes up.

Cost Analysis and Financing Parameters

Future trends and Investment Opportunity

Contingent consideration, often referred to as earnouts, is a strategic component frequently utilized in merger and acquisition (M&A) transactions. It is a financial arrangement wherein a portion of the purchase price is contingent upon the achievement of specific future performance metrics by the acquired company. In the dynamic landscape of business acquisitions, contingent consideration acts as a flexible financial arrangement that links future payments to the performance of the acquired company.

Reasons Behind the Use of Earnouts:

Risk Mitigation: Earnouts are commonly employed when there is uncertainty regarding the future performance of the acquired company. Sellers might opt for earnouts to share the risk with the buyer and ensure that the full purchase price is commensurate with the actual performance achieved.

Valuation Misalignment: In cases where the buyer and seller have differing opinions on the current value of the target company, contingent consideration allows both parties to compromise by tying a portion of the payment to future performance.

Alignment of Interests: Earnouts align the interests of the buyer and seller, as both parties have a vested interest in the success of the acquired business post-transaction. Sellers remain involved in the company’s performance, aiming to maximize the contingent payments.

Characterizing Contingent Considerations:

While contingent consideration arrangements are often used to achieve similar purposes and exhibit certain common characteristics, contingent consideration structures observed in practice come in many different forms that are designed to address the unique risks associated with each specific transaction. An earnout may be broadly characterized by the choice of the underlying metric or event which triggers the payment, the structure or payoff of the earnout, and the means by which the earnout is ultimately settled.

1-Underlying Metrics:

Underlying metrics refer to a measurement unit defined in the contingent consideration agreement, the value of which will determine the amount of the contingent consideration to be paid.

Typical Metrics Include:

Financial metrics: Revenue (in some cases in conjunction with minimum gross margin conditions), EBITDA, net income, and business metrics such as number of units sold, rental occupancy rates, etc.

Non-financial milestone events: regulatory approvals, resolution of legal disputes, execution of certain commercial contracts or retention of customers, closing of a future transaction, achievement of technical milestones (such as completion of a product launch, a stage of product development, certain software integration tasks, or a construction project), etc.

The choice of the underlying metric will affect the riskiness of the contingent consideration payoff cash flow and therefore the relevant discount rate. For example, the risk associated with certain nonfinancial milestone events (such as an earnout contingent on regulatory approval of a pharmaceutical drug) might typically not be influenced by movements in the markets and therefore such risks are diversifiable, leading to the use of a discount rate similar to the cost of debt of the obligor over the appropriate time horizon. In contrast, the risk associated with a financial metric will generally not be fully diversifiable, leading to the use of a discount rate that includes a risk premium for that financial metric’s exposure to systematic risk.

2-Payoff Structures

At one extreme, contingent consideration may be structured in a simple way as a fixed percentage of an underlying metric such as earnings or revenue (i.e., a linear payoff structure). At the other extreme, contingent consideration payoff structures may be complex, nonlinear functions of the underlying metric, including minimum thresholds below which no payment is made, a maximum payment cap, tiers with differing rates of payment per unit of improved performance, and/or carry-forward provisions that link payment in one time period to performance in other time periods.

The contingent consideration structure can have a substantial impact on the risk, degree of leverage, and discount rate to use in the valuation. Furthermore, similar to the distinction between diversifiable and non-diversifiable risk, the distinction between linear and nonlinear payoff structures is a key consideration when selecting the contingent consideration valuation methodology.

Examples of Payoff Structure:

While most earnouts are settled in cash, there are cases where settlement involves the transfer of other assets, equity, and/or liabilities. The way an earnout is settled may or may not have an impact on its fair value.

If the earnout payment is specified in monetary terms but settled through the transfer of other assets. Such an earnout is economically equivalent to an earnout settled in cash.

Eg: An earnout payment equal to 500 worth of the acquirer’s common shares if EBITDA earned in the first year exceeds 5,000.

However, specifying an earnout as a fixed number of the acquirer’s shares will impact the fair value of the earnout, and the valuation of such an earnout generally requires consideration of the fair value of the shares being transferred, the impact on the counterparty credit risk and the correlation between the value of the shares and the underlying metric.

Eg: An earnout payment equal to 500 common shares of the acquirer if EBITDA earned in the first year exceeds 5,000.

Valuation Methodologies

At the acquisition date, IND AS 103 – Business Combinations requires an acquiring company to report the contingent consideration at fair value as part of the purchase price in an M&A transaction. The three generally accepted valuation approaches to estimate the value of an asset or liability include the income approach, the market approach and the cost approach. Given that the income approach incorporates future expectations, it is typically the approach used to value contingent consideration. Within the income approach, there are two commonly used methods to value contingent consideration.

1.The scenario-based method (“SBM”)

The scenario-based method requires the identification of a set of outcomes (or scenarios) for the underlying metric or event and the payoffs associated with each outcome. The payoffs are then probability-weighted according to an assessment of the likelihood of each scenario. The probability-weighted payoffs are then discounted at the appropriate rate to calculate the expected present value of the contingent consideration.

2. The option pricing method (“OPM”)

Option-pricing models are mathematical tools used to estimate the value of options – financial contracts that give the holder the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specific period. The three most widely used option-pricing models for valuing contingent consideration are the Black-Scholes-Merton model, the binomial option pricing model, and the Monte Carlo simulation.

Selecting a Valuation Methodology

The SBM is appropriate for pricing contingent consideration when the risk of the underlying metric is largely diversifiable and there is linear payoff structure. In the case of a metric with only diversifiable risk, estimating, the SBM discount rate need to only address the time value of money (risk free rate) over the relevant time horizon and any counterparty credit risk.

In the case of a linear payoff structure, the structure does not change the risk of the underlying metric. In this case the discount rate must incorporate the required metric risk premium as well as the time value of money over the relevant time horizon and any counterparty credit risk.

In the case of a nonlinear payoff structure (for example, a structure with tiers, thresholds, caps, or path dependencies such as carry-forwards, roll-backs or cumulative targets) involving a contingent consideration metric with non-diversifiable risk, estimating the discount rate for the SBM cannot be easily intuited by the valuation specialist as the SBM discount rate must be adjusted for the risk of that nonlinear payoff structure. In such cases OPM methodology is appropriate for valuing contingent consideration. In such cases the OPM provides a framework by which the impact of the payoff structure on the non-diversifiable risk of the metric can be easily modelled.

Conclusion:

Earnouts can be challenging to structure, value, and account for. However, when the two parties are far apart on value, they can be a handy tool to bridge the gap. By aligning the interests of buyers and sellers and addressing uncertainties in post-acquisition performance, earnouts contribute to the success of strategic deals. As the landscape of M&A continues to evolve, contingent consideration is likely to remain a significant component in structuring deals and fostering collaboration between acquiring and selling entities. Understanding the characterizations and valuation methodologies associated with contingent considerations is crucial for both parties to navigate these complex financial arrangements successfully.

Hemendra has founded VBD Capital Advisors Pvt. Ltd. – specializing in debt syndication and distribution of insurance products.

Hemendra has been in financial services since 1994 working in organizations like Aarayaa Finstock Pvt. Ltd., V. B. Desai Financial Services Ltd. and Religare Capital Markets Ltd. He has significant experience in business development with strong client relationship and accessibility to various institutional investors. He leads in negotiating strategic alliances and debt structuring of transactions.

India has embarked on a transformative journey towards renewable energy, with a particular focus on solar power. As one of the fastest-growing economies globally, India faces significant energy demands. To address these while tackling environmental concerns, the country has placed renewable energy at the forefront of its agenda. In 2023, India held the third position globally in solar power generation, making a significant 5.9% contribution to the sector’s global growth

India’s renewable power capacity is set to double from 2022 to 2027, with solar PV accounting for three-quarters of the growth, considering the target of achieving net zero by 2050.

Key Policy and Regulatory Reforms aiding the Renewable Energy potential in India

Among renewable sources, solar energy stands out as a pivotal component of India’s energy transition strategy. The country’s solar sector has experienced exponential growth, driven by favorable policies, technological advancements, and increasing investment. India’s abundant sunlight makes it particularly conducive to solar power generation.

Solar Module Manufacturing

• Module Manufacturing capacity to grow 2.1 times by FY29 aided by PLI Scheme and Backward integration through production of Polysilicon, Wafers and Cells.

• China plus one to benefit Indian Solar Module Manufacturers due to rising demand from the US, EU, Africa and the Middle East.

• Indian Solar module exporters have seen a significant surge attributed primarily to the restrictions imposed by certain countries on Chinese Imports, thereby creating a supply gap and a notable opportunity for Indian players.

M&A Trends

• India accounted for 20% of Asia’s Renewable Energy M&A deal value in 2022 and 2023.

• The Energy sector saw a steep rise of 63% in deal value in 2023, being driven by large deals.

• Driven by India’s target of clean energy capacity of 500 GW by 2030, the solar energy sector has seen a 30-fold increase in M&A activity from 2014- 2023.

• Past trends and Government push for clean energy likely to drive M&A Activity upwards in 2024-25

Conclusion

India’s renewable energy and solar sectors are pivotal in the country’s quest for energy security, economic growth, and environmental sustainability. With ambitious targets and supportive policies, India continues to lead the global renewable energy transition, positioning itself as a key player in the solar energy landscape.

Valuation for the equity raise from IIFL Special Opportunities Fund, Standard Chartered Private Equity and Affirma Capital

Valuation for purchase of shares by Apax Partners

In the dynamic world of finance and investment, the integration of Environmental, Social, and Governance (ESG) factors into business valuation has become a paramount consideration. As the global business community grapples with the requirements of sustainability and responsible corporate practices, investors are increasingly recognizing the need to go beyond traditional financial metrics. This article explores the multifaceted realm of ESG, delving into its significance, the process of integrating these factors into business valuation, challenges encountered in this endeavour and the highlights of Business Responsibility and Sustainability Reporting (“BRSR”) Core which has been introduced recently.

Understanding ESG & Its Importance

ESG encompasses a triad of critical factors that collectively shape a company’s approach to sustainability, ethical practices, and corporate governance. Environmental criteria evaluate a company’s impact on the planet, social criteria gauge its relationships with stakeholders, and governance criteria assess the internal structures guiding decision-making. The importance of ESG lies in its ability to provide a holistic view of a company, reflecting its commitment to long-term resilience, ethical conduct, and positive societal impact. Investors are increasingly recognizing that companies with robust ESG practices are not only better equipped to manage risks but are also likely to be more resilient in the face of evolving market dynamics.

Source: FTSE Russel

Integration of ESG into Valuation

The integration of ESG factors into business valuation marks a paradigm shift in how companies are assessed for investment. Traditional valuation methods are being augmented with ESG considerations, as investors seek a more comprehensive understanding of a company’s performance and its ability to create long-term value. ESG integration involves analyzing a company’s ESG practices and assigning a quantitative value to these intangible factors. Below are ways to incorporate the ESG impact under the market and income approach:

The Market Approach:

To account for ESG considerations, valuation under the market approach should:

Identify and assess ESG practices for comparable companies and industries, then

Assess the performance of the subject company for such criteria, and

Calibrate the market inputs to the subject entity to take into account the relevant performance as compared to the comparable companies.

An example for adjusting the ESG factor under market approach is as follows:

A significant limitation of this method is that ESG data, disclosures, and rating systems are currently in their early stages of development, particularly for entities that are often private companies. Consequently, the scoring process is subjective, as different practitioners may assign varying weightings or scores to distinct ESG factors and practices implemented by companies.

The Income Approach:

To account for ESG considerations, valuation under the income approach should consider its impact on the discount rate or cash flows itself.

While discount rate adjustments can be used to incorporate ESG into the Discounted Cashflow approach (DCF), adjusting the discount rate may lead to double counting if beta values have reflected the market’s perspectives on ESG risks. A better way of integrating ESG factors in the DCF can be to adjust future cash flows. This helps the investor to integrate the company’s ESG factors into future cash flows and thus to focus on the relevant material issues. Depending on different industries and company performances, the translation of ESG factors to cash flow adjustments varies. Hence industry to industry lens is very critical since there is no standardized benchmark in ESG integration and adopting industry and company specific value drivers could help avoid the ambiguity of the cash flow adjustments. Some of the adjustments to be considered include:

The “E” factor can be incorporated by adjusting the cashflows with additional costs and Capex investments in carbon reduction initiatives and costs savings from adoption of energy/water saving technology.

The “S” factor can be incorporated through adjusting costs related to employee training programs, hiring contractual employees on a permanent basis, workplace safety measures and research and development investments to ensure quality and safe products among others.

The “G” factor can be incorporated through adjusting for fines or penalties imposed by regulatory authorities due to weak governance policies of companies.

An example for adjusting the ESG factor under income approach is as follows:

Issues in Integrating ESG Factors in Valuation

While the integration of ESG factors into business valuation is gaining momentum, it is not without its challenges. One key issue is the lack of standardized metrics and reporting frameworks, making it difficult for investors to compare ESG performance across companies. Additionally, there are concerns about “greenwashing,” where companies may overstate their ESG credentials to appear more attractive to investors. Striking a balance between qualitative and quantitative assessment poses another challenge, as some ESG factors are inherently subjective and context-dependent. Overcoming these challenges requires the development of standardized reporting practices, increased transparency, and ongoing dialogue between investors and companies.

BRSR Core Framework

Recent developments in the ESG landscape include the introduction of the BRSR Core Framework by SEBI, an extension of the existing BRSR framework which delves deeper into ESG integration by providing specific requirements for reporting and assurance. This framework aims to enhance transparency and accountability for companies and further elevate the role of ESG in business valuation.

Key Features of BRSR Core:

Specificity: The framework defines a specific set of ESG indicators that companies must report on, – covering environmental, social, and governance aspects. This specificity ensures consistency and comparability across companies, facilitating easier analysis and assessment for investors.

Assurance: BRSR Core introduces mandatory assurance requirements for a subset of reported ESG information. This independent verification enhances the credibility and reliability of ESG data, reducing the risk of greenwashing and building investor confidence.

Value Chain Focus: The framework extends beyond a company’s own operations to include its value chain, requiring reporting on the sustainability practices of its suppliers and partners. This broader scope provides a more comprehensive picture of a company’s overall impact and promotes responsible sourcing practices.

Phased Implementation: BRSR Core’s implementation is phased, starting with the top 1000 listed entities by market capitalization. This gradual approach allows companies to adapt and implement the framework while minimizing disruption.

Impact on Business Valuation:

Enhanced Data for Valuation Models: The BRSR Core’s specific and assured ESG data provides valuable input for valuation models, enabling a more comprehensive assessment of a company’s long-term value and risk profile.

Better Risk Assessment: Deeper insights into a company’s ESG performance through the value chain helps identify potential environmental, social, and governance risks that could impact financial performance.

Improved Comparability: The standardized reporting and assurance requirements facilitate easier comparison of ESG performance across companies, enabling investors to make more informed investment decisions based on ESG considerations.

BRSR Core represents a significant step towards a more integrated and transparent ESG landscape. The BRSR Core framework is still evolving, and its impact on business valuation is likely to grow as companies adapt and investors refine their assessment methods. Ongoing collaboration between regulators, investors, companies, and valuation professionals is crucial to ensure the effectiveness and continued improvement of the framework. Addressing data availability and accessibility, particularly for smaller companies, remains a challenge that needs to be tackled to ensure fair and equitable application of the framework.

Conclusion

In conclusion, the integration of ESG factors into business valuation is a transformative trend that reflects the evolving priorities of investors and the broader business ecosystem. ESG considerations are no longer peripheral but integral to evaluating a company’s overall performance and potential for sustained success. While challenges persist, the ongoing evolution of reporting frameworks like BRSR signals a commitment to addressing these issues and advancing the integration of ESG into mainstream financial practices. As businesses navigate this new landscape, embracing ESG not only contributes to a more sustainable future but also positions companies as leaders in an era where responsible practices are synonymous with long-term value creation.

With almost 20 years of investment banking experience, Nirav has been successfully involved in various transactions including Private Equity, M&A (International & Domestic) and Corporate Finance. He has worked on all stages of a transaction from Deal Origination to Execution and Closure. He has been a part of the early team at Aarayaa and has been instrumental in multiple successful deals across Automotive, Aerospace & Defense, IT & ITES, Engineering & Industrials, Consumer etc.

He has earned his MBA degree from Warnborough College University, U.K. and also holds a Bachelor’s degree in Commerce from Mumbai University.

Saurabh joined Aarayaa in the year 2009 and is actively involved in valuation and merger & acquisition projects.

He is a graduate of Commerce from NarseeMonjee College of Commerce & Economics, M. Com, MBA in Finance from Thakur Institute of Management Studies & Research (TIMSR) and Company Secretary (C.S.).

He is also a visiting faculty at Malini Kishore Sanghvi College (Ritumbhara College), TIMSR etc.